The dermatology and aesthetic markets have been defined by new relevant factors over the past 18 months as a result of the pandemic. This includes temporary practice shutdowns, the reopening and resurgence of dermatology and aesthetic operations, and the adoption of alternative practice methods and solutions. Regardless of challenges and changes, consumers have continued to value what dermatology and aesthetics providers have to offer. The strength and attractiveness of these industries is evidenced by the robust mergers and acquisitions and capital placement activity in these health care segments. Understanding the new trends helps strengthen the dermatology and aesthetics markets, as well as shape practice decisions for the future.

The Pandemic: Adjustments & Solutions

COVID-19’s invasion of North America in the early Spring of 2020 negatively impacted most industries, and the dermatology and aesthetic markets were no exception. The International Dermoscopy Society completed a survey of 678 dermatologists regarding the impact of the pandemic, and 334 respondents stated COVID-19 had caused a reduction of more than 75 percent in daily work activity during the pandemic.1Dan Rodgers, President of Skin and Aesthetic Centers, a Midwest-based, multi-location dermatology group, comments, “To survive the pandemic, I think every industry was challenged to hone efficiencies and reinvent their approach to the marketplace. Very few were tested as heavily as the aesthetic space, as mandatory shutdowns on elective procedures forced cosmetic heavy practices to pivot quickly to maintain even minimal cash flows.” To combat the challenges, dermatology and aesthetics groups had to adopt creative means to service patients and drive performance.

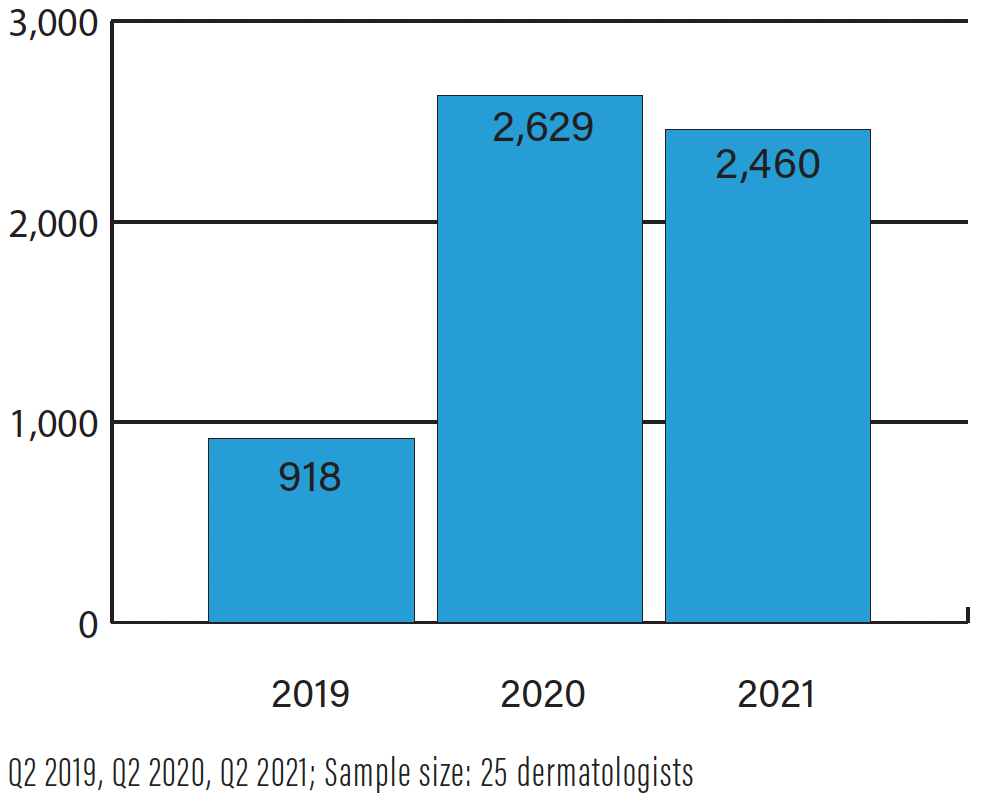

Figure 1: NEXTPatient: Average Monthly Appointments Booked Online

The use of new technologies and services demonstrated providers could embrace the adage of “necessity is the mother of invention.” Mr. Rodgers further comments, “Ambitious plastic surgeons stepped into complex closures for Mohs and reconstructive surgeries, and dermatologists leaned into telemedicine and even provided cosmetic consults over video conferencing.” On the technology solutions front, and as highlighted in the International Dermoscopy Society survey, nearly 20 percent of dermatologists utilized telehealth solutions for the first time.1NextPatient, a technology firm that partners with dermatology and aesthetic practices to allow patients to book online, witnessed an accelerated adoption in online scheduling technology. “Out of necessity, the pandemic drove patients to begin evaluating their health care provider under consumer-like terms, including whether a provider’s scheduling availability is online,” says Kyle Morham, co-founder of NextPatient. “As a result of this change in patient behavior, we’ve seen an undeniable shift in practices’ buying attitude and adoption of online scheduling.”

A third example of a technology-enabled provider is MedShift, which provides equipment, monitoring, and data analytics solutions to dermatology and aesthetic providers. “Practices and device manufacturers—both unable to service patients and providers in person—investigated and purchased solutions to continue business in a technology forward, remote-oriented manner,” states Brian Phillips, Chief Executive Officer of MedShift. “During and following the period of COVID-forced downtime, MedShift’s eCommerce and Payment Facilitation platform demand surged 740 percent, which enabled practices to sell vital products online to patients, and to allow manufacturers the ability to sell products to practices without in-person sales team interaction,” he adds.

Today, the performance of many dermatology and aesthetic practices suggests the impact of the pandemic is shifting, and providers are seeing evidence of more predictable performance. Patient visits have increased substantially, which reinforces that a visit to the dermatologist remains a critical healthcare expenditure. Many physician groups continue their use of creative technologies and solutions to service patients and enhance margins. It is evident the value of these segments is strong and very well positioned for the future.

Dermatology and Aesthetics Mergers and Acquisitions Markets: Continued Momentum

尽管全球大流行,整合和investment in the dermatology and aesthetic markets have remained progressively solid. This acquisition and investment activity over the past decade has largely been driven by financial sponsors, which include private equity groups and family offices. While COVID-19 may have created a moment of pause for these investors, their optimism for these segments and their growth opportunities was not broken. These sophisticated capital sources have found the dermatology and aesthetics markets to be a safe haven to place money into, including in a time of uncertainty.

In spring 2020, the dermatology M&A market experienced a “reflection moment” for buyers. This occurred as buyers had to assess the impact of the shutdowns on the state of potential dermatology investment candidates and their respective financials. With the uncertainty of the pandemic still active in summer 2020, the ability of most practice buyers to value, underwrite, and close transactions remained somewhat unsettled. However, in parallel with practices quickly learning how to operate in this new normal and the reopening of health care facilities with increasing patient visit counts, the financial performance of many were regaining their footing by fall 2020. As a result, the ability of buyers to close on transactions was revitalized.

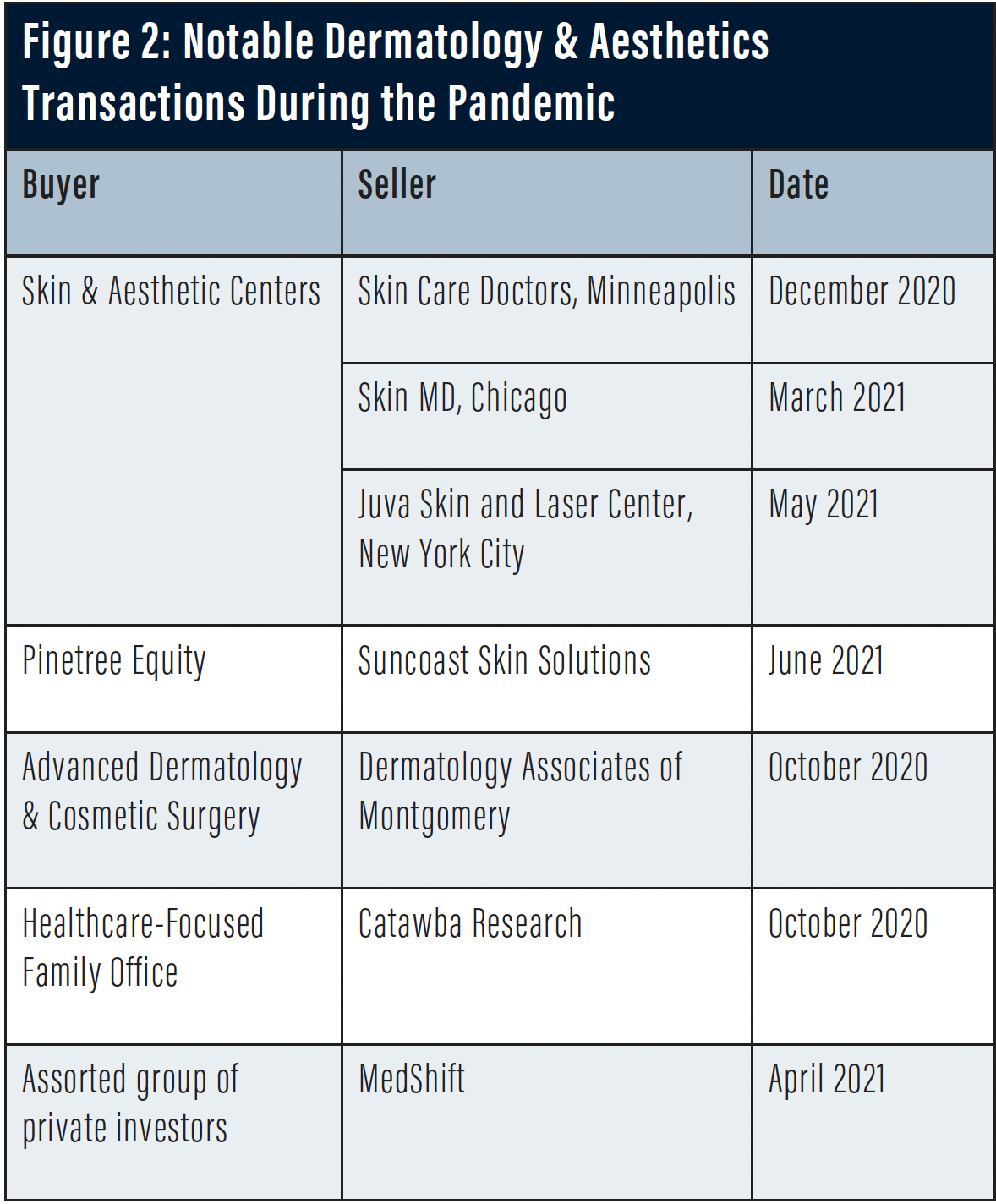

“Our team, backed by Abacus Investments and Citibank, was deep into diligence on our first tranche of partnerships as COVID peaked. It was amazing to watch these physician groups adjust, and it was clear that the dermatology and aesthetic sectors were illustrating that resilience that inspires investors,” says Mr. Rodgers. “Skin and Aesthetic Centers closed on three partnerships between December of 2020 and May of 2021: Skin Care Doctors, Minneapolis; Skin MD, Chicago; and Juva Skin and Laser Center in New York City. Not only have these practices bounced back, but all are tracking to exceed pre-COVID revenues.”

With 2021 now over the halfway mark, and with many practices either back to normal performance or within striking distance of normal, there is continued M&A and investment momentum in the dermatology and aesthetics markets. A number of high-profile dermatology transactions closed from mid-2020 through Summer of 2021, proving the continued lure of capital to these segments (see Figure 2). Examples include Pine Tree Equity’s investment in Suncoast Skin Solutions, ADCS’ acquisition of Dermatology Associates of Montgomery, and the expected sale of Forefront Dermatology, one the largest national dermatology and aesthetics groups, in the near future. In short, the buyer’s market and robust valuations have returned to pre-pandemic levels, and one might argue the overall value of these segments, and the physician practice groups within it, has increased post-COVID.

Technology Solutions for Physician Practice Groups

Physician practice groups will continue to be the backbone of the dermatology and aesthetics markets. Buyers and financial sponsors are expanding their interest in technology-oriented firms that provide solutions to physician practice groups. The rapid adoption of new technology-oriented services to physicians include telehealth, virtual bookings, and data analytics. The investment community is responding in-kind, as daily transaction announcements in the health care technology are occurring.

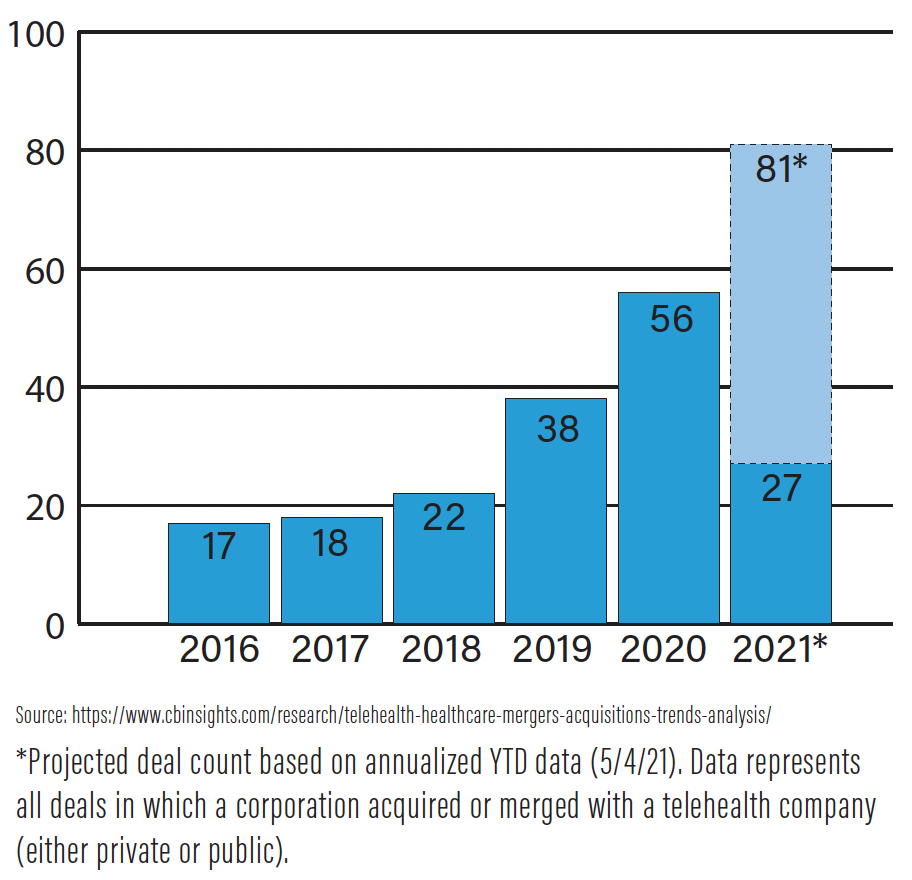

资本flowin的最近的一个例子g into technology-oriented companies focused on the dermatology and aesthetics market is MedShift. The company recently received strong interest in a minority equity capital raise, resulting in an oversubscribed funding round at a company valuation of $150MM. Further evidence of interest is observed by M&A trends in the telehealth segment, which witnessed an increase from 22 transactions in 2018 to a projected 81 in 2021.2From Bundy Group’s continued health care technology-oriented firms, we see an escalation in financial sponsor interest in any firm that offers proprietary technology solutions for health care providers. The marriage of physician practice services and technology results in highly attractive value drivers and a magnet for both strategic buyers financial sponsors. We expect these health care technology firms to continue to demand great value and interest from the investment community.

Figure 3: Telehealth M&A Activity (2016 – YTD 2021)

The Future of the Dermatology Market

Dermatology and aesthetics practices have proven they can weather a major storm and generate continued buyer and investor interest, as evidenced in the 2020/2021 rebound and resurgence. From Bundy Group client engagements in the dermatology and aesthetics industries, we have seen firsthand the continued growth of these markets and the corresponding premium valuations that can accompany independent physician practices. Not only has the value been retained by most dermatology and aesthetics independent practices, but it looks to be stronger than ever. Furthermore, technology-oriented firms servicing the health care and physician practice management markets are also demanding significant attention. Any independent physician practice group, or technology-focused health care firm, considering a sale or recapitalization, will have plenty of options and be in a great position to demand value—especially with the use of competitive pressure on buyers in a structured process.

Bundy Group represented Catawba research and Dermatology Associates of Montgomery in transactions and has provided advisory services to SkinMD.

克林特·邦迪与邦迪集团董事总经理p, a boutique investment bank with an extensive track record in the dermatology and health care markets. Since 1989, Bundy Group has specialized in representing practice and business owners in business sales, capital raises and acquisitions. www.bundygroup.com;clint@bundygroup.com

1. Conforti C, Lallas A, Argenziano G, Dianzani C, Di Meo N, Giuffrida R, Kittler H, Malvehy J, Marghoob AA, Soyer HP, Zalaudek I. (2021, January) Impact of the COVID-19 pandemic on dermatology practice worldwide: results of a survey promoted by the International Dermoscopy Society. Dermatol Pract Concept. 2021;11(1):e2021153.https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7875667/

2. CB Insights. (2021, May 6). Telehealth cos are seeing a wave of consolidation. Here’s what that means for the future of virtual care. CB Insights Research. https://www.cbinsights.com/research/telehealth-healthcare-mergers-acquisitions-trends-analysis/.